Wealth is the product of man’s capacity to think. – Ayn Rand

The Financial Intelligence Factor

The Financial Intelligence Factor is state of mind, that comes from being a certain way and doing certain things that attract wealth and abundance into your life.

This IQ Matrix is based on Jamie McIntyre’s best selling books and DVD entitled “What I Didn’t Learn at School but I Wish I Had.” Within this material, Jamie discusses financial strategies and techniques that will help you build towards financial freedom.

Jamie’s book and DVD cover a great breadth of wealth creation topics that simply cannot all be covered on a single map. However, for the purpose of this discussion, we will break down and identify some of the key strategies and techniques that Jamie used to rid himself of $150,000 of debt that eventually paved the way to multi-millions of dollars and financial peace of mind.

As you progress through this information you will come to know the characteristics of a competent and incompetent money manager; the mentality of success and failure; how to identify limiting beliefs that could be sabotaging your money earning potential, and guidelines for designing your financial life in ways that will focus and direct you towards your primary wealth creation goals. Moreover, the mind map breaks down some simple financial knowledge and strategies that will help you build long-term wealth while pinpointing the strategies that Jamie uses every single day to earn an extraordinary amount of money.

This post will be a combination of my commentary coupled together with direct quotes and insights from Jamie’s best selling book.

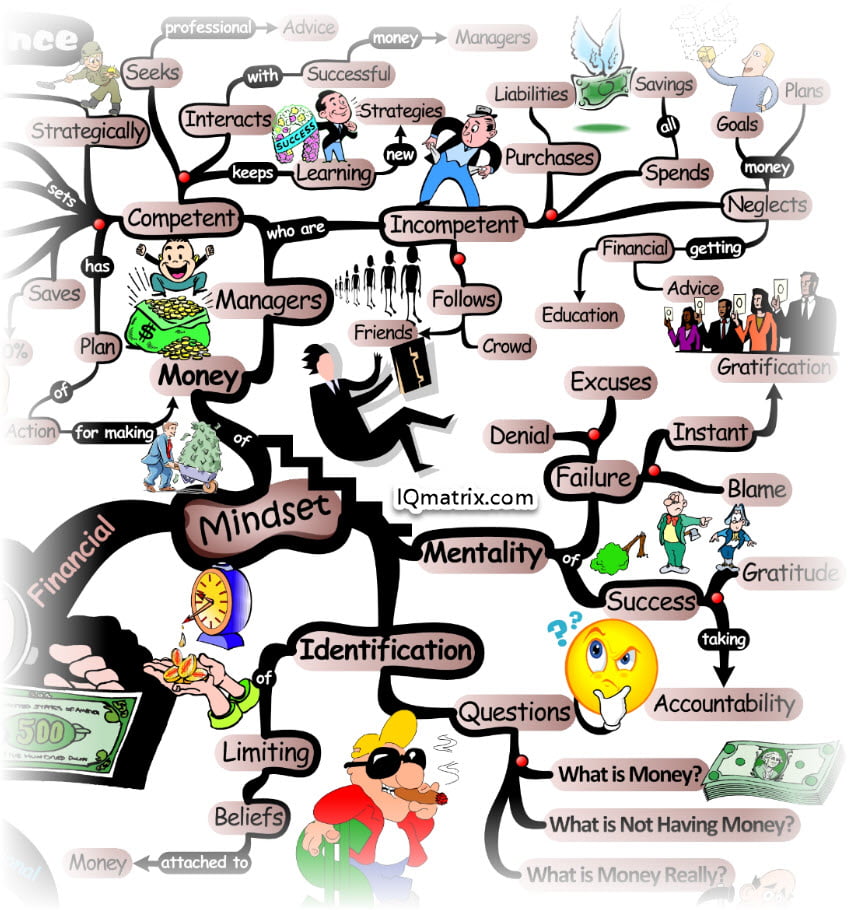

The Mindset of the Financially Intelligent

Jamie learned the hard way when he realized that there are certain and specific actions that competent money managers take in order to build vast amounts of financial wealth and abundance. This naturally leads to an understanding of the differences between the mentalities of the financially successful and the financially poor of this world. These two findings came together to reveal that our financial success is very much governed by the underlying beliefs we have about money. The premise is, that if we continue to hold limiting beliefs about money, then we will likewise continue to suffer the consequences of holding onto these self-sabotaging forces that will prevent us from ever reaching the pinnacles of financial freedom.

Competent Money Manager Characteristics

This list of characteristics are common amongst those who have a long proven history of earning high amounts of money.

Has Plan of Action

Financially intelligent people create a comprehensive financial plan of action that they manage and implement on a daily basis.

Saves 10% of Income

Financially intelligent people consistently save at the very least 10% of their earned income and utilize it for investment purposes or compound their money for long-term gains.

Minimizes Purchasing Liabilities

Financially intelligent people understand the burden of liabilities and how this can affect their long-term wealth. Hence, they minimize purchasing liabilities. However, if they must purchase liabilities, then they will search for the best and lowest price before making a purchase decision. Often liabilities are purchased from the profit earned from smart investments.

Sets Long and Short-term Money Goals

Money goals work hand-in-hand with an effective plan of action. Goals provide these people with both short and long-term objectives that keep them focused and motivated throughout their day.

Strategically Spends Money

Each and every purchase that financially intelligent people make is thought through carefully.

Great money managers understand the long-term consequences of making even the smallest purchase decisions. They know that an accumulation of seemingly insignificant small purchase decisions will usually result in long-term consequences that will either add to their debt or provide them with opportunities to earn profits.

The financially intelligent have an uncanny ability to see into the future. Utilizing the act of foresight to help identify the possible consequences that can potentially result from each spending decision they make, they determine if the consequences are justifiable. If long-term profits don’t result, then they will carefully weigh-up their decision before taking any further action.

Seeks Professional Financial Advice

Financially intelligent people understand that they don’t know it all. Hence they seek professional advice from experts who have a long history of financial success.

Interacts with Successful Money Managers

To become a great money manager, one must learn to absorb the characteristics, habits and daily rituals of those who have succeeded before them. For this reason, competent money managers interact and socialize with successful money managers. They understand that through each interaction they will gain deeper insights and knowledge that could be critical to their next major financial decision.

Keeps Learning New Money Strategies

Financially intelligent people simply never stop learning about money, finances, investments, property, shares, etc. For them, money is as natural as breathing air. Every moment throughout their day they are either listening to an audio program about wealth, reading a book, speaking to others about money, attending a financial seminar, reading the finance section of the daily paper and more. Money is a way of life, which is why they are financially successful.

Has money become a way of life for you?

Incompetent Money Manager Characteristics

On the other side of the coin, we have the majority of people who can be labeled as incompetent money managers. Identify if you have any of the following financially sabotaging traits.

Constantly Purchases Liabilities

The competent money managers avoid purchasing liabilities at all costs. On the other hand, incompetent money managers seem to be magnetically pulled towards the temptation of wonderfully packaged and emotionally charged liabilities that will lose them a significant amount of money in the long-term.

Spends all Savings

Incompetent money managers will purchase anything at any time whenever they feel the urge to spend. They are emotional creatures who enjoy the feeling of spending, and the resulting emotions of instant gratification. Hence, they live from paycheck to paycheck. When money comes in, they spend. When money is not available, they either hold back on their expenses or redirect their spending habits onto their credit cards.

Neglects Money Goals and Plans

Incompetent money managers don’t put enough importance on having money in their lives, which is why they simply neglect to set goals and create a financial plan of action to move them away from debt and into financial freedom.

Neglects Getting Professional Financial Advice

First of all, they don’t believe that they require any help when it comes to making effective financial decisions that will secure their future.

Secondly, they can’t justify paying money to a good financial advisor without first seeing the results in their bank accounts. Unfortunately, the world doesn’t work this way. They have to learn to understand that they must spend money in order to earn money long-term. However, their spending of money must come in the form of self-education and advice that will set them along the right path.

Many of these people simply don’t believe in their ability to follow through with the action steps that will be necessary to obtain financial freedom. In such instances, they just don’t have enough commitment behind their actions. And therefore they will continue to languish in debt until they find the necessary motivation to pull themselves through.

Neglects Getting a Financial Education

Incompetent money managers simply don’t see a need in obtaining a good financial education. This stems from the belief that they don’t seem to perceive money as an important enough factor in their lives.

These types of people also prefer to rely on little hunches to carry them towards financial freedom.

Follows Friends and Crowd

To an incompetent money manager, any tip is a good tip. It’s therefore not unusual for them to gather around with their friends and discuss financial matters, often sharing tips and stories. Not only does everyone within this group have a poor financial background, but what’s worse, is that they will follow their friend’s advice (or the masses) blindly without ever questioning their decision.

The downside of this strategy is that the masses (this usually includes their friends) belong to the 96% of the population who are incompetent money managers. So even though this advice is free, it will cost them more in the long-run. They simply forget that nothing is free if you weigh up the long-term consequences of each decision. This is especially true when it comes to earning your financial freedom.

Mentality of Success

There are two key characteristics that Jamie identifies within his book and DVD that separate the successful people from the rest.

Accountability

Jamie says:

until now I have been making excuses and shifting blame. Once I applied the law of opposites, I discovered that if I was going to make it financially and in any other area of my life, I needed to be accountable. Once I accepted I was responsible for my mistakes, I was able to reclaim my personal power… Along with accountability comes action.

Gratitude

Jamie points out that his millionaire mentor once told him:

Jamie, if you want to be successful, here is what I recommend you do. Every morning when you wake up, find five things that you can be grateful for in your life. You may need to train yourself to focus on what you can be grateful for, because without gratitude you will never have true wealth.

Mentality of Failure

On the other side of the coin, we have the failure-centered mentality, which affects the vast majority of our population.

Here are some characteristics of this type of mentality that you must avoid at all costs.

Instant Gratification

If you are the kind of person who seeks instant gratification in life, then becoming financially free is unfortunately not going to be on your tarot cards (unless you get lucky and win the lottery). Instant gratification is a silent killer that will keep you in debt — or just above the poverty line — for as long as you stay hypnotized within its subtle spell.

Denial

Jamie points out:

I used to say, “I am not interested in money — money is not everything.” Until my millionaire mentor told me that I was in denial. I could not figure out what he meant by this. He said, “Jamie, do you think if you say you are not interested in money then that is going to help you become financially successful?” and I thought, “Well, no, maybe not.”

Living in denial is another silent killer that will continue to sabotage your financial success for as long as you continue to live in that place of being.

Blame and Excuses

Jamie points out:

that the other two important qualities you need to have in order to be in the 96% of people who fail financially, is the ability to blame everyone else for your problems and to create elaborate excuses. I become really good at blaming other people when things were not working for me. Not only did I blame other people but also the circumstances.

Identifying Limiting Beliefs about Money

Statistics show that many of us will unfortunately never obtain financial freedom. The main reason for this is that the majority of people have a plethora of self-sabotaging beliefs pertaining to money that will keep them in the doldrums of day-to-day survival.

Jamie mentions within his book some strategies that can assist you with identifying these limiting beliefs that you hold about money and ridding yourself of them once and for all.

To begin with, get someone to ask you the following set of questions. It is not specifically the answer that is important, but rather the memory associated with your answer that could potentially pinpoint the origin of your limiting beliefs.

What is money?

What is not having money?

What is money really?

Attracting Financial Abundance Intentionally

It is said that “If you fail to plan, you are simply planning to fail“. When it comes to obtaining financial freedom, there is probably right on the money. 😉

In this section, we will discuss simple, yet very effective strategies, that will help you to design your life intentionally and set you on target towards your financial objectives.

First, and foremost, you must establish your purpose. Secondly, you must set effective goals that will keep you on target and moving toward your objectives. And finally, in order to become emotionally and financially intelligent, we must all learn to master some fundamental skills that are essential towards creating an abundance of wealth in our lives.

Determine Your Primary Life Purpose

No financial dreams can truly be achieved if we do not first become clear on our purpose. Jame says:

This is probably the most important step, because unless you have clarity on what you want, then no amount of strategies will help you get what you want.

Jamie lists a set of questions that we should be asking ourselves in order to clarify our life’s purpose.

Here is a list of four questions you should ask yourself in order to determine what it is that you really desire from your life. You will only gain from this exercise by being completely honest and genuine in your responses.

What do I not want in my life?

What do I want in my life?

What are my priorities?

What challenges do I currently face?

Write Your Primary Purpose Down on Paper

Jamie instructs:

to write a very short statement — a phrase, a sentence, no more than a couple of sentences — expressing the essence of what you want your life to be all about. The acid test for your primary purpose is your internal barometer. When you write it, you should feel energy, enthusiasm, commitment, a sense of “Yes! This is it for me!” If you do not feel this, keep on writing.

Set Effective Financial Goals

As we mentioned earlier, setting effective financial goals is a process undertaken by competent money managers who succeed financially in life. There are several methods and processes of setting and structuring your goals. Jamie identifies a very simple and effective method that you can use immediately to create powerful action-oriented objectives. Here is Jamie’s breakdown of the process:

Specific

Be absolutely specific when setting your goals, and use only the present tense positive statements.

Measurable

Your goals need to be measurable, in other words, you need to be able to monitor your progress so you can measure your success.

Attainable

You also need to be able to conceive your goal in order to attain it. Unless you can see yourself achieving your goal, it is very unlikely to happen.

Realistic

Obviously goals need to be within the bounds of logic and circumstance.

Tangible

Your goal needs to be something that is real or physical, that you can see and touch.

Inspirational

If your goals do not inspire you, it is unrealistic to expect that you will be driven to take action to achieve them.

Emotional

The more emotionally involved you become with your goal the quicker it will manifest into your life.

Master the Skills that will Enhance Emotional and Financial Intelligence

Both emotional intelligence and financial intelligences are of primary importance if you seek to obtain financial freedom in your life. Jamie defines emotional intelligence as:

having the ability to consciously respond to a situation rather than react under the influence of our emotions at that time.

On the other hand, financial intelligence is something that is obtained from knowledge and experience gained from working with money. All of the mindset strategies, characteristics, money habits, and technical tools discussed within this post add to your financial IQ.

On top of these intelligences there are also four critical skill areas that Jamie sees as being of critical importance towards the achievement of long-term financial success. Here is a breakdown of these key skill areas in Jamie’s own words:

Creative Thinking

Of the four key areas that I have worked on during the last eight years of my life the first is the ability to think. What I mean by thinking creatively is having the ability to solve challenges.

Negotiating

The second area we need to nurture is the ability to negotiate. In life to get what we want we have to know how to negotiate. If you want to be successful, the secret is to never take no for an answer.

Communicating

The third skill is the ability to communicate. If you cannot communicate a benefit to someone else so that they can understand it, then you are not communicating effectively and will not achieve your desired result.

Marketing

The fourth area is the ability to market or marketing. I am talking about result-focused marketing. How do you take an idea or concept and communicate that message in a business format to the marketplace to make it a reality?

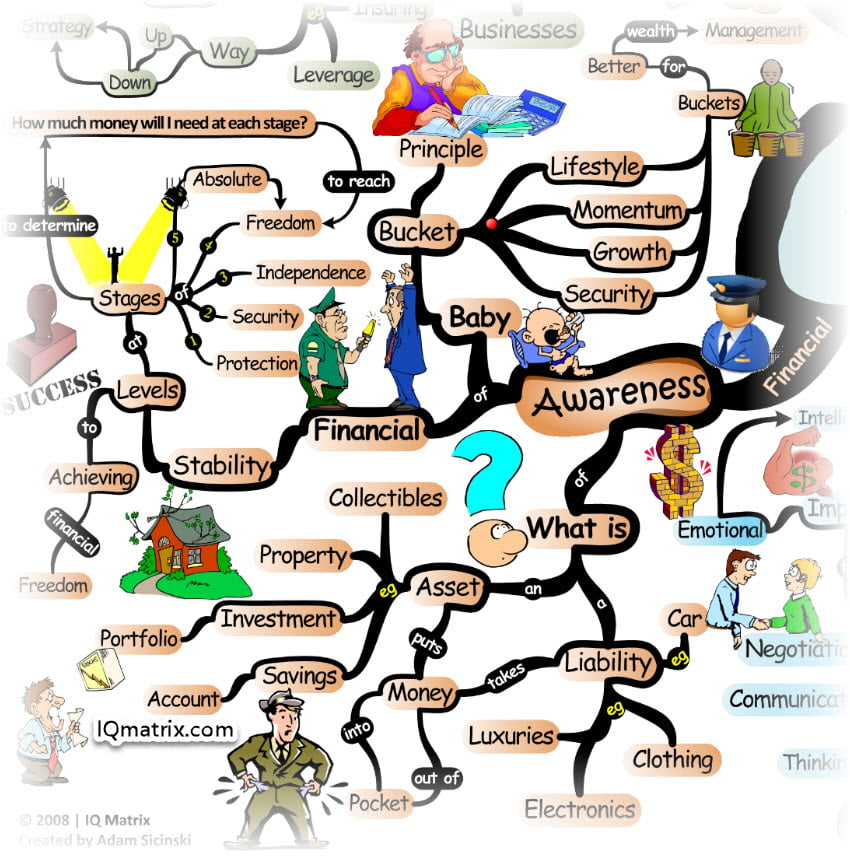

Becoming Financially Aware

Financial education and awareness go hand-in-hand to help us better manage our finances. This section will touch upon some very effective learnings and strategies that are important to know and understand before you begin moving along your path towards obtaining your financial freedom.

What is a Liability?

A liability is simply anything that takes money out of your pocket in the short or long-term. Liabilities are pretty much anything that you purchase that loses you money or depreciates over time. These kinds of purchases can include clothes, electronics, gadgets, cars, and other luxuries.

What is an Asset?

An asset is simply something that puts money into your pocket. It is basically something that will bring you a financial return over the short or long-term. Assets can include collectibles, investment portfolios, property or even savings accounts.

Determining Your Financial Stability Levels

Jamie calls these the Levels of Financial Well-being. He states that these levels are possible to attain by anyone who has discipline and a passion to reach the pinnacle of absolute financial freedom.

Within his book, Jamie discusses the process in significant detail. However, for the purpose of this post, we will just quickly examine (using Jamie’s words) what each of these financial levels mean for each of us. Bear in mind, that each level requires a different set of tasks and objectives that you must strive for.

Financial Protection

The precise amount of money you will require in liquid assets to be financially protected can be established simply by reviewing your current monthly overheads.

These overheads can include mortgage payments, electricity, gas, transportation, food, insurance, and the total monthly income that you will need to secure your protection. These will give you the basic requirements that are necessary for your financial survival.

Financial Security

This is the amount of money you will need to achieve financial security. This means determining how much you need to be independent of the basic necessities such as food, clothes, and transport. Financial security is achieved when your investments produce an income equal to your financial protection figure… you would have calculated above.

Financial Independence

This means determining the money you will need to be financially independent of work. How much money do you now earn annually? To duplicate your current lifestyle, it is likely you will need to duplicate your present monthly annual income.

Financial Freedom

This goal is attained when your investments provide enough income for you to live the lifestyle you desire for the rest of your life without ever having to work again. Simply ask yourself, “What annual income would I need to have the lifestyle I want?

Within his book, Jamie provides instructions on how to best calculate this level of financial well-being.

Absolute Financial Freedom

You have achieved absolute financial freedom when your investment income provides you with the certainty that you can do whatever you want, as much as you want, whenever you want, with whomever you want, — without ever working again.

The Baby Bucket Principle

This is a very effective financial management strategy that will progressively move you up the financial well-being ladder. A similar approach was discussed within the wealth management IQ Matrix. The process is pretty much the same, however, Jamie puts his own unique twist on the bucket principle. Let’s take a look at how the process works in his own words.

Security Bucket

This is for low risk investments. These include cash management trust accounts, i.e., physical cash, 404k, and superannuation. You would include insurance. I suggest income protection, disability, and health, you need to consider those sorts of insurances if you become an active borrower for investing to lower your risk in case you lose your job while building your wealth or suffer illness.

Growth Bucket

This includes residential property, quality companies, renting, etc., are investments that belong in this bucket.

Momentum Bucket

This would cover renting, commercial property, investing in traditional business, etc. However, do not borrow for a business until you can afford to lose the money.

Lifestyle Bucket

Here you are investing in your personal lifestyle such as a resort, holiday, farm, or lifestyle business.

Strategies for Making Money

Within the previous sections, we discussed effective ways to manage your money, along with providing you with some strategies and tools that naturally focus and direct your mind towards wealth and abundance.

Within the final section, we will bring everything full circle and discuss specific strategies that Jamie uses on a daily basis to create financial abundance in his life.

Investing through the Banks

Your first and safest option is to invest and earn an income through the banking system. Jamie points out that,

if you put your money in the bank, the cash interest rates may be between 4 and (if you are lucky) 6 percent, so it is going to take a lot of money to become wealthy. That is why many people think that they need to win lotto, because if they have a million dollars from lotto and they receive a 5 or 6 percent return on that money, then they will have $50,000 – $60,000 per year to replace their income.

Investing in Businesses

Jamie warns others to be cautious when investing in business. He says,

if you have been in business for more than five years, do not get too excited as the next five years after that 80 percent of those businesses will fail. One thing I have noticed is a big mistake many have made. What they will do is borrow money out of their house in a line of credit and use that money to commence a traditional business. Often that traditional business fails and as a result these people lose the business and possibly the house as well — it all ends in a total financial disaster. Before investing into a business, keep in mind that a true business is a profitable enterprise that will work ideally without you.

The Investment Risk Pyramid

This pyramid structure will provide you with a quick overview of the variable risks associated with specific types of investments. When starting out you should consider using conservative strategies, and slowly progressing toward aggressive and high-risk tactics that could potentially bring forth higher returns.

Conservative Strategies

These strategies include Government Bonds, Debt Money Market, Bank Accounts, Cd’s Notes, Bills Bankers Accept, Cash and Cash Equivalents.

Aggressive Strategies

These strategies include Real Estate, Equity Mutual Funds, Large and Small CapStocks, High Income Bonds / Debt.

High-Risk Strategies

These strategies include Options, Futures, Collectables.

Share Market Strategies

Jamie has had a vast amount of personal success investing in the share market. He points out that it is important to take charge of your money and educate yourself on how to make effective investment decisions. He says that,

I did not become wealthy as a self-made millionaire by going and sitting in front of a financial planner. Actually, I would not have become a millionaire by following their advice. Why would I do that if they are not successful investors themselves? My millionaire mentor told me the obvious question to ask of financial planners is, if they could help me to become financially independent and live my ideal lifestyle, then why are they not doing it themselves? What you want to look for in learning financial success is to learn from people who have produced results, not people who just have a license to give advice on money, because anyone can get a license to advise on money without the need to be an investor themselves.

Jamie presents some investments strategies he uses in order to create financial abundance. The following is a brief overview of these strategies.

Forms of Analysis

The first strategy that a potential investor may consider is commonly called technical analysis. Here you examine patterns of share price changes and changes to the volume of shares traded in the hope of being able to predict and profit from future trends.

Channelling

The second strategy for investors is something I call channelling. For the technically minded, this strategy is referring to the price range of a share, that is, the price range between the highest and lowest price reached by a share during any specific day, week or year. By following the charts of many companies’, one can visually identify that the price range of a share will move in patterns.

Leverage

The third strategy for investors is a concept termed leverage. Leverage is another word for gearing, which in its simplest format is the process of increasing the funds available for investment through borrowing. Leverage has the potential to increase returns as the more money that is invested in the market, the greater the potential return from dividends and other distributions inclusive of capital growth in a share.

Insuring

The fourth strategy for investors is a concept I call insuring. Entering into an insurance premium is simply the right to sell a share at a specified price before the expiry date of the option. Insurance allows investors to hedge against a possible fall in the value of shares in their portfolio. After taking out some insurance, the sale of our imaginary share is locked in for the term of the insurance no matter how low our imaginary share price may fall.

The Way Down Strategy

This concept refers to buying insurance without owning the share. The purpose of this investment strategy is to speculate that the share price will fall. Investors see this concept as a way of making money without owning the share. Investors understand that when the price of the share falls, the value of the insurance premium increases. Therefore, an investor will purchase an insurance contract with the intention of selling the insurance at a higher price.

The Way Up and Down Strategy

This concept is similar to the way down strategy. The main difference is that the investor has a view that the share price will move upwards and therefore a rental contract is purchased. A rental contract gives an investor the right to buy the underlying share for a pre-determined value. Investors therefore use the purchase of a rental contract when they believe that share price will rise and the investor wants to benefit from the share price movement.

Investment Property Strategies

Investing in property is a popular investment strategy that Jamie highly recommends as an effective tool for building long-term wealth. However, he again cautions others that this must be done in the correct manner in order to gain maximum benefit and returns from the time, money and energy you spend.

Within his book, Jamie discusses a number of ways that one can earn money through renovation, adding value, selecting the right property (checklist), renting out and more.

Other Strategies for Making Money

We will end our discussion with a quick look at five useful strategies that will either save you money or provide you with the extra income you need to pursue your investment objectives.

We all have to start somewhere, and not having enough money should never be an excuse for not pursuing your journey towards becoming a great investor. Here is Jamie’s take on these five strategies.

Improving Habits of Saving

All great investors are great savers. If you are not saving money now then you are never going to become wealthy until you start saving.

Selling Stuff

To make extra money, could you sell something? What I am suggesting is that you could have a garage sale. Are there some things that you no longer need or are willing to sacrifice in the short-term to set yourself up financially. Anything that you could convert to cash to come up with a few thousand dollars is great.

Cutting Taxes

The third step is tax minimization. Look for ways to minimize your taxes in order to use that extra money for investment purposes. Within his book, Jamie pinpoints some simple, yet effective ways you can go about doing this.

Increasing Your Income

If you can increase your income by an extra 10 percent, that is an extra 10 percent you could put aside for savings and investment. To create wealth, my millionaire mentor always said, “Jamie you must add more value. One way you can do that is to improve and develop your skills.”

Here Jamie suggests focussing on the four skills of creative thinking, communication, negotiation and marketing that we discussed a little earlier.

Utilizing Equity Sensibly

Many people have equity in their homes, equity being a portion of their house they actually own. Much of that equity could be put to good use, rather than just sitting there idle. I suggest using some of that equity to invest in investments that are going to generate some cash-flow.

Concluding Thoughts

I hope that after reading this you feel more confident in your ability to build towards obtaining financial freedom in your life.

Jamie has proved that these strategies work, however they do require patience, commitment and some sacrifice to bring the results you desire to fruition.

Time to Assimilate these Concepts

Did you gain value from this article? Is it important that you know and understand this topic? Would you like to optimize how you think about this topic? Would you like a method for applying these ideas to your life?

If you answered yes to any of these questions, then I’m confident you will gain tremendous value from using the accompanying IQ Matrix for coaching or self-coaching purposes. This mind map provides you with a quick visual overview of the article you just read. The branches, interlinking ideas, and images model how the brain thinks and processes information. It’s kind of like implanting a thought into your brain – an upgrade of sorts that optimizes how you think about these concepts and ideas. 🙂

Recommended IQ Matrix Bundles

If you’re intrigued by the idea of using mind maps for self-improvement then I would like to invite you to become an IQ Matrix Member.

If you’re new to mind mapping or just want to check things out, then register for the Free 12 Month Membership Program. There you will gain access to over 90 mind maps, visual tools, and resources valued at over $500.

If, on the other hand, you want access to an ever-growing library of 100s of visual tools and resources, then check out our Premium Membership Packages. These packages provide you with the ultimate visual reference library for all your personal development needs.

Gain More Knowledge…

Here are some additional links and resources that will help you learn more about this topic:

- 20 + Free Passive Income Resources @ Life Optimizer

- 7 Steps for Starting a Financial Checkup @ Scott H Young

- 78 Timeless Wealth Building Tips from Benjamin Franklin @ Pick the Brain

- How to Conquer Your Fear of Investing @ Get Rich Slowly

- A Few Tools to Help You Invest @ Lifehack

- 5 Frugality Hacks Straight Out of the Great Depression @ Wise Bread

- 9 Methods for Mastering Your Money @ Get Rich Slowly

- Investing 101: An Introduction to Index Funds & Passive Investing @ Get Rich Slowly

- How to Make Lots of Money During a Recession @ Steve Pavlina