Money is only a tool. It will take you wherever you wish, but it will not replace you as the driver. – Ayn Rand

This article is part of a series of five articles that will help you to make more effective and sound financial decisions. Here is a list of all articles within this series:

- A Common Sense Guide for Getting Out of Financial Debt

- A Practical Guide for Saving Money

- Ideas to Help You Live More Frugally and Save Money

- Common Sense Guidelines for Managing Money

- Simple Guidelines for Building Long-term Wealth

I’m not a financial planner and so there are no investment guidelines and certainly no stock market predictions to be found within these articles. These articles simply present you with common sense practical ideas to help you become more financially savvy.

Understanding Your Financial Position

If you desire to gain control over your finances and begin building toward financial freedom, then the very first step you need to take is to get your financial life in order. What this essentially means is gaining clarity about your current financial position. This would typically include listing down:

- How much income you’re currently earning weekly, monthly, quarterly and annually.

- How many expenses you have and what these expenses are costing you weekly, monthly, quarterly and annually.

- What investments you currently have, the value of those investments, and potentially the interest you are earning from these investments.

- What debts you have owing to specific creditors and potentially how much interest you are paying on those debts.

- How much money you have saved, which would typically include how much disposable and discretionary income you have on hand.

In addition to these points, it’s also important to get an overview of your spending habits. It’s only when you take the time to analyze how you’re spending your money that you get a sense of where potential savings can be made.

The purpose of undergoing this financial analysis process is to take back control of your financial life. It’s about identifying what’s working, what’s not working and where you might be overextending yourself. As a result, you will be in a far better position to prioritize accordingly and make more optimal financial decisions moving forward.

How to Begin Shaking Up Your Financial Life

Having gained a clearer picture of the health of your finances, it’s now time to start making more optimal decisions that can help you get ahead.

Within this article, we will spend the majority of our time breaking down the importance of budgeting and of establishing an emergency fund. Addressing these two key areas will help you manage your finances far more effectively. However, before we even begin exploring these areas it’s important to address some indispensable financial habits that will be of value.

Each of the financial habits listed below are designed to challenge you to think about money a little differently. Adopting these habits into your life will help you to begin making smarter and more optimal decisions about your finances.

You will, of course, find nothing revolutionary here. These are common sense habits that we all inherently know and understand. However, understanding something is very different to actually taking the time to adopt it into our lives. As such, I would suggest spending a little time thinking about each of the following habits and identifying how they could potentially be of value.

Here is the list of key financial habits that will help you begin managing your money far more effectively. I have listed these habits in the form of statements. Simply answer whether or not each statement is true or false in your situation.

- Saving money is a top priority in my life.

- I always save for irregular and unexpected expenses.

- I strive to eliminate my debts as quickly as possible.

- I avoid purchasing on credit and/or spending money I don’t have.

- I avoid borrowing money that I will realistically struggle to pay off.

- I avoid getting myself into recurring payment cycles that dry up my cash flow.

- I pay my bills together at the same time every month to better help manage my cash flow.

- I avoid taking out unnecessary insurance that I will realistically never need.

- I have an emergency fund in place that I can use to keep myself afloat when my financial circumstances suddenly change.

- I don’t make rash financial decisions. I always carefully evaluate my options before making a purchase or investment.

- I always endeavor to learn from the financial mistakes I make, and subsequently make more optimal financial decisions down the road.

- I have a solid financial plan and budget in place that lays out how I plan to build toward financial freedom in the coming years.

If you answered “true” to all of these statements, then you’re well on your way toward securing your financial future. On the other hand, if your financial habits are the opposite to what’s listed above, then the chances are that you are probably currently struggling financially.

The key to learning how to manage your money more effectively begins with developing solid habits that will help you make more optimal financial decisions. The above mentioned financial habits are a great place to start. However, there are two habits in particular that are of significant value here. Adopting these two habits will put you in the right financial frame-of-mind to help you begin building a more secure financial future.

The habits I’m of course referring to come in the form of budgeting and of establishing an emergency fund. Let’s break these two habits down into detail below.

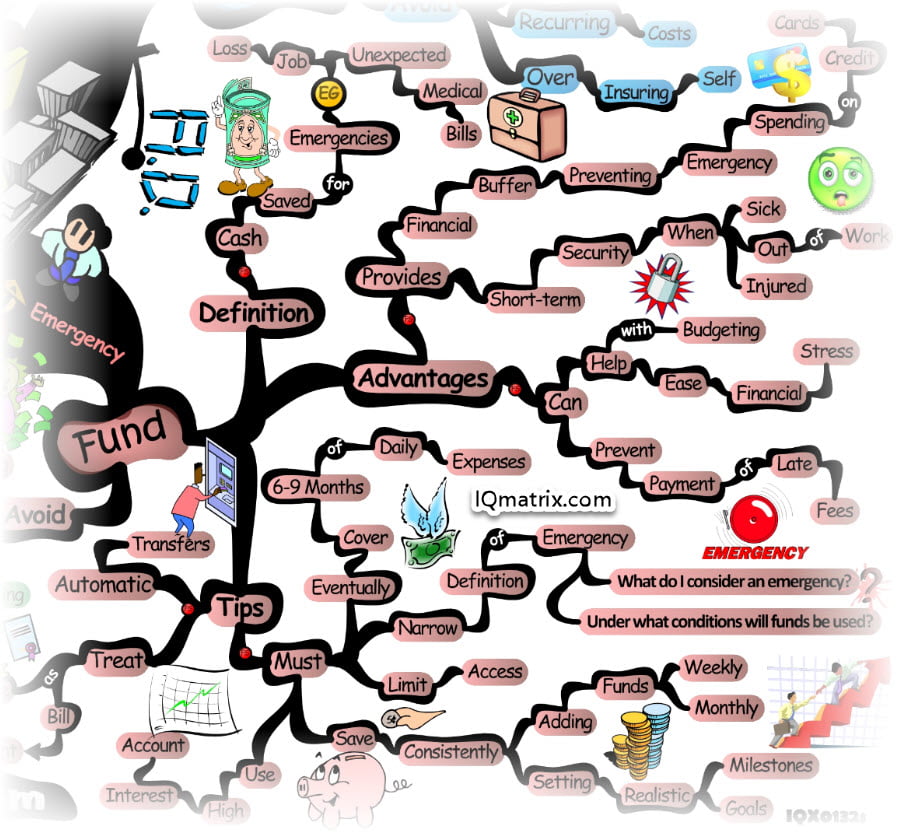

The Value of Creating an Emergency Fund

An emergency fund is essentially somewhat like a savings account. It’s cash you save for emergencies such as for unexpected medical bills, accidents, or for when you’re out of work for an extended period of time.

An emergency fund is however not the same as a savings account. A savings (or income) account you use freely to make everyday purchases. An emergency fund, on the other hand, is a fund for cash that you don’t access unless something unexpected happens that is deemed an “emergency”.

The advantage of having an emergency fund is that it provides you with a financial buffer that will prevent you from using your credit cards. Moreover, it’s something that will help ease your financial burden when Murphy’s Law suddenly kicks in. 🙁 It will essentially help reduce the financial stress you experience when significant and unexpected expenses arise. Furthermore, an emergency fund goes hand-in-hand with budgeting, which is something we will discuss a little later in this article.

Ideally, you will want to open a high interest-bearing bank account that you will use for your emergency fund. After setting some realistic goals and milestones, your objective will be to add cash to this account each week or month. Treat it like a regular bill payment that you make to yourself. You can even set up automatic bank transfers that transfer a certain amount of cash from your income account to your emergency fund.

Your target is to store a minimum of 6 to 9 months of disposable income into this fund. What this essentially means is that you must have enough funds in this account to cover all your living expenses for a period of 6 to 9 months.

How to Use Your Emergency Fund

Let’s say for instance you lost your job and couldn’t work for a period of 6 months. Most people in this situation could survive but would rack up a significant amount of debt on their credit cards. However, with 6 months of emergency cash to work with, you can use that money for living expenses while you figure out how to get back into the workforce. As a result, you will avoid getting into the financial debt.

In another scenario, your emergency fund comes in handy when significant and/or unexpected expenses suddenly arise. Again, most people will typically dig deep into their credit cards to cover these expenses, and as a result, rack up unnecessary debt. You, on the other hand, can simply dig deep into your cash reserves.

This is, of course, all well and good, but what is an emergency really? How will you know whether something is or isn’t a legitimate emergency? Well, this is precisely what you will need to define. Ask yourself:

What do I consider to be an emergency?

Under what specific conditions will I use my emergency fund?

Emergencies are typically unexpected expenses that arise suddenly, that disrupt your cash flow, and cost you a small fortune. For instance, the roof of your house caves in, or maybe you are involved in a car accident, or possibly you fall sick and miss a significant amount of time at work without any pay, or just maybe one of your kids breaks a leg and needs to be treated in hospital, or possibly a water pipe bursts and floods your home, etc.

These are all unexpected emergencies that arise and disrupt your cash flow. Typically these are the scenarios where you would normally want to access your emergency fund. However, it is up to you to define precisely under what conditions you will use these funds, and then commit yourself to this agreement.

Many times you may very well be tempted to dig into your emergency fund to purchase a new car or to fund an unforgettable holiday. These are not emergency expenses. If you use these funds for purchasing luxuries, then you may very quickly regret your decision when a legitimate emergency arises and you simply don’t have the funds to pay for it.

Your emergency fund is essentially an insurance policy you take out on unexpected emergencies. Yes, I realize many people have home and contents insurance, health insurance, and car insurance, however, life is also full of many other emergencies that these insurance policies do not cover. Moreover, your insurance will only cover you up to a certain point. Anything beyond that point, you will need to fund yourself.

Having an emergency fund in place gives you peace of mind. You have that quiet sense of assurance that no matter what happens you will be ready and prepared to deal with the financial consequences that may result. But you must, of course, be very diligent not to spend this money on addictions, on luxuries or on weekly shopping excursions. And above all else, do not lend it out to family or friends. This is your emergency fund. Nobody else needs to know that it even exists.

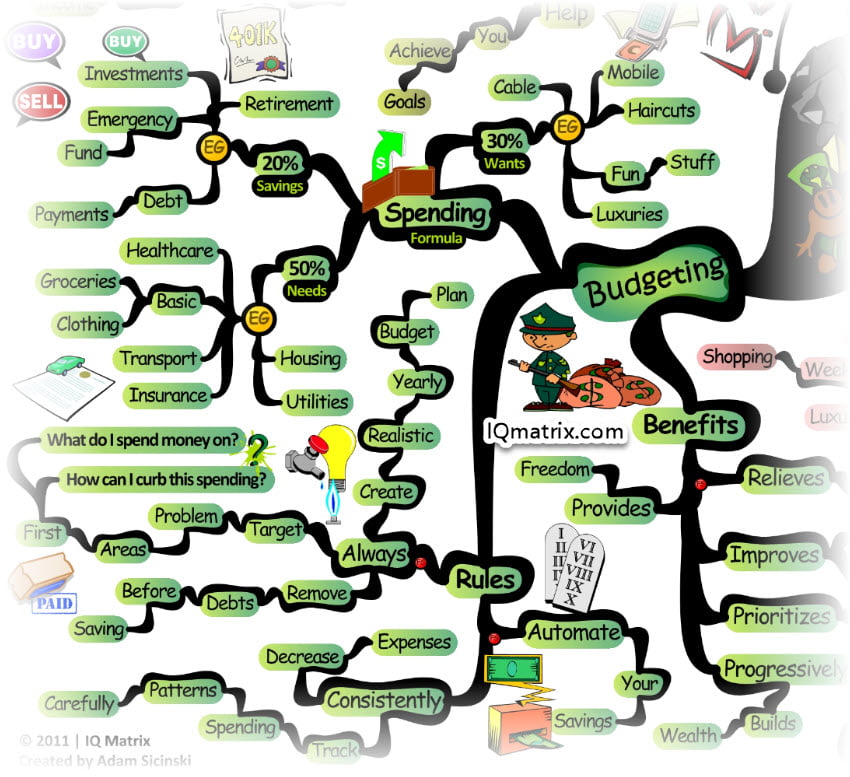

The Incredible Value of Budgeting

Along with establishing an emergency fund, budgeting is another key financial habit that can be of tremendous value.

Budgeting essentially involves assigning very specific amounts of money for spending on certain living expenses each week and month. However, it’s not only about spending but also about saving and investing.

A standard budget breakdown will typically follow the 50/30/20 rule. The income you receive every month you will spit in the following way:

- 50% will be spent on NEEDS. This includes housing, utilities, healthcare, basic clothing and groceries, transportation and insurance.

- 30% will be spent on WANTS. This could include cable television, mobile phone, the internet, haircuts, fun stuff and various luxuries that you may want to buy.

- 20% will be spent on SAVINGS. This includes your emergency and retirement funds, making debt payments, as-well-as funding investments.

There are of course many variations of what a great budget formula looks like. The “percentage spread” within this formula might work well for some, but not so well for others.

If for instance, you are in financial debt then it’s important to allocate as many funds as possible to pay off that debt. Or let’s say for instance you don’t yet have a large enough emergency fund to support you for 6 to 9 months, then you will possibly want to reduce your spending on WANTS to 10% and allocate 40% of your income to the SAVINGS category.

Setting up a workable budget requires making some common sense decisions that fully accounts for the financial situation you currently find yourself in.

Your first objective is to always allocate money to pay for your NEEDS. Your next objective after that is to get yourself out of financial debt, followed by establishing an adequately sized emergency fund that can support you for up to 9 months. Only once you have these areas covered should you start focusing on your WANTS.

Once you have an effective budget in place you will typically find that you experience less financial stress. As a result, you are able to think more clearly about your spending habits, and this, therefore, improves your ability to make more optimal financial decisions.

7 Rules for Building an Effective Budget Plan

An effective budget involves putting in place a realistic plan of action that will guide the financial decisions you make throughout the course of a year. Setting up this budget plan requires adhering to the following rules:

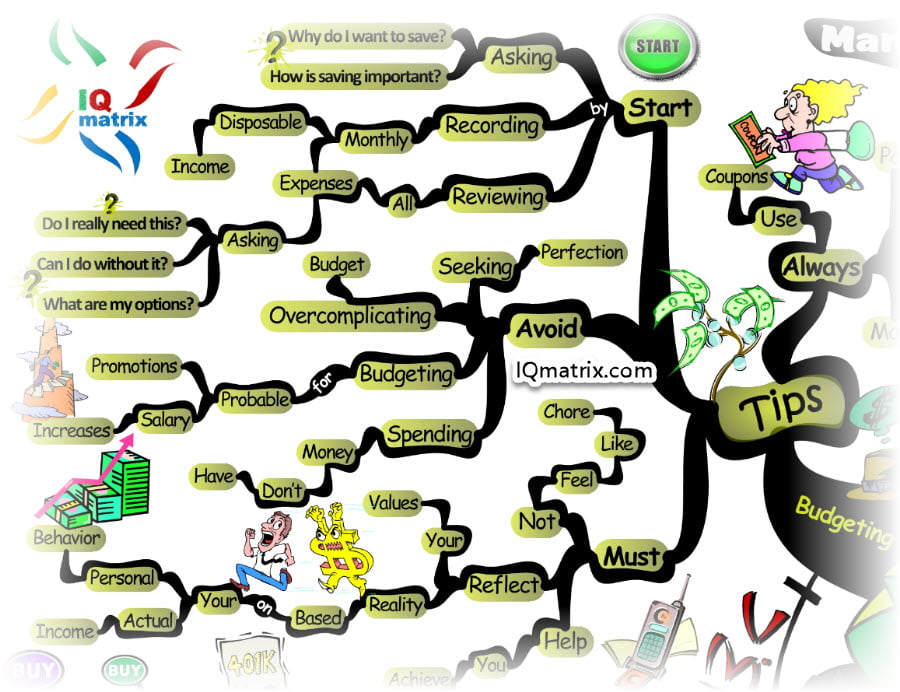

Rule 1: Track Your Spending

You must establish a method for tracking your daily, weekly and monthly expenses. This, of course, involves understanding your spending patterns and figuring out where all your money is going. I personally use YNAB for this purpose.

Rule 2: Allocate Funds Carefully

You must allocate money toward paying off your debts before building your savings or emergency fund. However, the exception to the rule is that you need to pay yourself first in order to substantially cover all your NEEDS.

Rule 3: Minimize Your Monthly Expenses

You must consistently figure out ways to minimize your monthly expenses. In other words, identify and target problem areas where you could curb your spending.

Three key questions to ask yourself that will help you to adhere to this rule are:

Do I really need this?

Can I do without it?

What are my options?

Rule 4: Save Whenever Possible

Figure out ways you can save money wherever possible. This, of course, means allocating as many funds into your SAVINGS budgeting category, as is needed. The more funds you can allocate here the stronger your long-term financial position.

To get you into the right frame-of-mind, ask yourself:

Why do I want to start saving?

Why is saving money important to me?

What’s the long-term value of getting into this habit?

Keep in mind that saving includes allocating money to your emergency fund, retirement fund, and into various investments. I have also included debt in this category because it’s typically something you will want to pay off first before investing money elsewhere.

Rule 5: Only Spend Your Own Money

You must avoid spending money that isn’t yours. Whatever money you have on hand or in your bank account is money you must allocate accordingly. Your credit cards are not part of the equation.

One practice that will make following this rule easier is to only carry cash. If you don’t have the cash on hand to pay for something, then simply move on and maybe purchase it another time.

Rule 6: Don’t Budget for Possibilities

You must avoid budgeting for possible promotions or salary increases. Unless you actually have the money in the bank, then it shouldn’t be part of your budget plan.

Rule 7: Be Flexible in Your Approach

You must be flexible in your approach. When your circumstances change you must be willing to adjust your budget and change your approach wherever necessary.

Following these seven rules is a great start, however, it’s also important to keep in mind that the budget you create must essentially reflect your values and the reality of your financial situation.

Budgeting must also not feel like a chore, but rather an extension of your desire to improve yourself and your life. You are however not seeking perfection here. Keep your budget simple, practical and yet flexible enough to adapt to changing conditions and circumstances. Over complicating things will only bog you down and prevent you from making sound financial decisions.

Concluding Thoughts

Budgeting will require a little work on your part, and it’s something that you will need to persevere with over the long-haul. However, your perseverance will eventually pay off and provide you with more financial flexibility. Moreover, it will go a long way toward helping you build a solid platform for getting your financial life in order.

Time to Assimilate these Concepts

Did you gain value from this article? Is it important that you know and understand this topic? Would you like to optimize how you think about this topic? Would you like a method for applying these ideas to your life?

If you answered yes to any of these questions, then I’m confident you will gain tremendous value from using the accompanying IQ Matrix for coaching or self-coaching purposes. This mind map provides you with a quick visual overview of the article you just read. The branches, interlinking ideas, and images model how the brain thinks and processes information. It’s kind of like implanting a thought into your brain – an upgrade of sorts that optimizes how you think about these concepts and ideas. 🙂

Recommended IQ Matrix Bundles

If you’re intrigued by the idea of using mind maps for self-improvement then I would like to invite you to become an IQ Matrix Member.

If you’re new to mind mapping or just want to check things out, then register for the Free 12 Month Membership Program. There you will gain access to over 90 mind maps, visual tools, and resources valued at over $500.

If, on the other hand, you want access to an ever-growing library of 100s of visual tools and resources, then check out our Premium Membership Packages. These packages provide you with the ultimate visual reference library for all your personal development needs.

Gain More Knowledge…

Here are some additional links and resources that will help you learn more about this topic:

- 6 Simple Strategies for Better Money Management @ Entrepreneur

- 10 Common Money Management Mistakes You’re Probably Making @ Forbes

- 15 Ways Millionaires Manage their Money that Make them Richer @ Entrepreneur

- 77 Reasons You’re Aweful at Managing Money @ Huffington Post

- A Practically Painless Guide to Managing Money @ Forbes

- How to Manage Your Finances Without an Adviser @ Time

- How You Should Manage Your Money and Keep it Short @ NY Times

- In Your 30s or 40s? What You Need to Know About Managing Money @ CS Monitor

- Managing Your Money: 12 Things Every Woman Should Know @ Huffington Post

- Managing Your Money, Managing Your Life: Part 1, Part 2, Part 3 @ Forbes

- Managing Your Money When You Lose Your Job @ Forbes

- The Basics of Money Management @ Entrepreneur

- The Only 7 Things You Really Need to Know About Managing Money @ Greatist

- The Ultimate Guide to Managing Money in Your 20s @ Greatist