It takes as much imagination to create debt as to create income. – Leonard Orr

This article is part of a series of five articles that will help you to make more effective and sound financial decisions. Here is a list of all articles within this series:

- A Common Sense Guide for Getting Out of Financial Debt

- A Practical Guide for Saving Money

- Ideas to Help You Live More Frugally and Save Money

- Common Sense Guidelines for Managing Money

- Simple Guidelines for Building Long-term Wealth

I’m not a financial planner and so there are no investment guidelines and certainly no stock market predictions to be found within these articles. These articles simply present you with common sense practical ideas to help you become more financially savvy.

The Consequences of Living in Financial Debt

Statistically speaking, the chances are that you are currently in financial debt. You might have a student loan, a car loan, a home loan, or credit card debt to pay off. For some people, debt isn’t much of a problem. As long as more income is coming in each month than is leaving your pocket, then you’re probably doing fine, for now… until that layoff or that unexpected crisis, car accident or horrendous medical bill.

Most people can successfully manage small amounts of debt, however, it’s when something unexpected happens that makes us overextend ourselves financially, that is when we struggle to stay afloat. That is when small debts become big debts that are difficult to overcome.

At other times our debts kind of just pile up over a period of time. First, it’s that expensive brand new outfit for that special dinner party you’re attending for your “uncle’s friend’s sister’s boyfriend’s birthday.” 😉

Next, it’s that temptation to buy that flashy phone or purchase the latest gadget on your credit card. Then there’s possibly a small personal loan for a new car. Then there are more birthdays, anniversaries and celebrations. And all these gifts just get piled onto your credit card.

At the time you, of course, acknowledge that when your next paycheck comes in, that all these debts will magically disappear. 🙂 But even before that paycheck arrives you tempt yourself to purchase those new shoes and you splurge on an expensive night-out on the town. And then, of course, there’s that holiday you planned with your family, which you currently can’t afford, but you lay down a deposit anyways. The chances are you will have the money eventually, right?

You justify all these expenses because you believe that you will eventually pay these things off. And even if you don’t quite pay it all off with your next paycheck, you will certainly do it the following month. Yes, you’ll pay some interest on your credit card, but it’s only a little. You’re not worried. You have everything under control, right?

Well, possibly you do, but the chances are you probably don’t. The longer you persist with this spending spree the more likely you are to develop the habit of spending money that doesn’t belong to you. And then one day when you least expect it something unfathomable will happen that will force you to dig even deeper into your credit card debt — just to keep yourself afloat. And now, not only are your credit cards almost maxed out, but there is also uncertainty about how you will pay your rent, or even put food on the table.

Struggling to pay off your debts you worry about being chased by collection agencies. As a result, you suffer from high amounts of stress and anxiety. And on top of this your standard of living progressively diminishes, which leads to restless and sleepless nights worrying about where you will find the money to get your life back on track.

To think, that you actually envy those with no home and no debt to their name. They are after all in a much better financial position than you. If only you could start over again. 🙁

How Eliminating Debt Starts in Your Head

I could give you a plethora of practical ideas to help you eliminate debt, however, these ideas simply won’t stick. You won’t follow through on them because you are not in the right frame-of-mind to work your way out of debt. As such, debt elimination always begins in your head. It begins with cultivating the mindset required that will help you to make sound financial decisions moving forward.

Adopting this mindset, however, won’t be easy. It will possibly require you to break some deeply ingrained habits that no longer serve you moving forward. This is tough and will take some time, but if you commit yourself to making these changes, then anything is possible.

So, a commitment to making a change is the first step. Your next step is to stop your whining and complaining. More importantly, leave your excuses at the door. It doesn’t matter what happened. It doesn’t matter what mistakes were made, and it certainly doesn’t matter who wronged you or influenced you into this financial mess. Just stop making excuses and start taking responsibility for your life and circumstances.

Unless you take responsibility for your financial decisions, you will never take the initiative to make positive changes. Change comes only through responsibility. And it doesn’t matter “who did what to you” or whether or not you had the power to influence their decisions. The past is the past. Leave it there, and get on with your life in the present moment. By owning your problems you start taking ownership of your life. Only then can you start making positive changes to help you get out of financial debt.

Once you have committed to making changes and taken ownership of your problems, it’s now easy to get overly excited and start making some rash decisions that might possibly get you into further debt. I’m of course talking about those “get rich quick schemes” that way too many people get sucked into. These schemes are not realistic and won’t save you. Yes, statistically speaking some people succeed and end up in a better financial position than when they started, but for the vast majority, it’s only a path to further debt.

Instead of jumping onto the new “financial craze”, choose instead to bide your time. Cultivate patience, optimism, discipline, creativity, courage, and perseverance. These are the attributes that will help you to make sound financial decisions moving forward. Moreover, they are the attributes that will allow you to successfully work through the seven-step debt elimination process outlined below.

The Seven Step Debt Elimination Process

What follows is a seven-step process you can use to help you progressively get out of debt. This is by no means a miracle cure to your situation. Everyone’s predicament is different and it will, therefore, take longer for some than for others to work their way out of debt.

Moreover, it will take a great deal of time and effort on your part to work through each step successfully. All the while, you will need to cultivate the six attributes listed above. These attributes are the key ingredients that will help you to take the necessary actions required to get yourself out of debt.

As you move through these steps do keep in mind that some sacrifices will need to be made. You can’t realistically eliminate your debt without making sacrifices. And of course, the chances are it will hurt. Making these sacrifices will be difficult to do. But things must be sacrificed in order to help you move your life forward in a more optimal way.

Step 1: Acknowledge Your Problem

Your first step is to openly acknowledge that you are in financial debt. In fact, take full responsibility and ownership of this problem. Whether you were directly or indirectly involved, one way or another you are to blame for this. Given a second chance you would probably do things differently, and as a result, you would make a different set of choices along the way. As such, this is your problem and your burden to bear.

Seeing your debt as a problem is also quite helpful. Problems are things that come with solutions. Every problem comes with a solution that can be implemented. In fact, it probably comes with a plethora of solutions that will help you dig your way out of debt.

Acknowledging that you have a problem helps you get into the necessary frame-of-mind for solving that problem.

Step 2: Take Inventory

Once you have taken ownership of your financial debt, it’s now time to take an inventory. What I mean by this is to simply list all your debts. With knowledge, of course, comes power. Knowing who you owe and what you owe helps you to take control of your financial decisions.

To begin with, list all your debts from lowest to highest. Next, figure out how much money you will allocate to paying off these debts each week or month. The key here is to pay off your lowest debts first, thereby whittling down the number of creditors you owe money to. The fewer creditors on your books, the less likely debt collection agencies will be hunting you down.

In addition to this, contact your creditors to ask for a payment plan or for an extension of your payments. Moreover, if you’re paying interest, ask if they could potentially lower your fees indefinitely or for a limited time.

Step 3: Eliminate all Non-Essentials

Now that you have a debt elimination plan in place, let’s look at ways to save some money to help you pay off your debts more quickly.

In step 3 of this process, make a list of all non-essential items you regularly purchase that could very much be classified as “comfort items”. For instance, those chocolates and biscuits, or how about those dance classes, or the gym membership? Yes, your health is important, but you can also stay fit and healthy from home.

Take time to list absolutely everything that you just don’t need to survive. You will, of course, need to make some tough decisions here, and some members of your family might not be very happy, but sacrifices must be made. The sooner you can pay off your debts, the sooner you can progressively re-introduce these things back into your life.

Consider also the cost of petrol while driving to work. Possibly using public transport will be a much more cost-effective method of transportation. Yes, it might be inconvenient, but is it as inconvenient as owing a massive amount of debt to a bunch of creditors banging on your door? It certainly helps to put everything into perspective. 🙂

Step 4: Create a Realistic Spending Plan

Your next step is to create a realistic spending plan to help you save money and live more frugally. I’m of course talking about a budget plan where you set daily, weekly and monthly spending limits on categories of items that you need to survive.

It’s important that you are very stringent with the limits you set. You will often find that you can live on far less than you thought might have been possible. It may just take a little work, effort, and creativity to pull it off.

You might, for instance, need to sacrifice purchasing the “big brand names” and instead purchase more affordable variations of that product. Or you may instead choose to purchase items that are discounted. We will discuss specific ideas on how to save money and live more frugally within other articles within this series.

Step 5: Sell all Unnecessary Items

Let’s now pay off some of the smaller debts quickly by putting more cash in your pocket. To do this, make a list of all the things that you kind of don’t need and can sell for a quick buck.

Whether you sell these items online, or just open your garage to the public and ask them to name their price, doesn’t matter. What matters is that you get as much money into your pocket as quickly as possible.

With this money on hand, be careful though how you spend it. Yes, certainly pay off your smallest debts to begin with, but also consider how having cash on hand can help with standard living expenses. After all, it’s much easier to budget and control your spending with a limited amount of cash in your pocket, then it is with a plastic card in your hand. 🙂

Step 6: Figure Out How to Increase Your Income

Now comes the fun part. Within Step 6 of this process, you need to start thinking creatively about various ways you can increase your income to help you pay off your debts far more quickly.

Yes, you may very well have a full-time job, and yes you also have all these other responsibilities at home. However, if you are unable to pay off your debts, then you might not have a home to live in for very much longer. As such, this step becomes of paramount importance. And with all things considered, you are probably much more resourceful than you give yourself credit for.

In order to increase your income consider the possibility of working longer hours on your job. Or how about working a second job after hours several nights per week — just until you get your feet back on the ground?

If you’re self-employed, then consider how you might be able to provide more value to your customers. Or how about figuring out how to earn more per customer transaction? Or how about increasing the number of transactions? Or how about restructuring your pricing or changing the product or service you offer in some way?

I’m sure there are many options that you could consider. Use some creativity and ask your family and friends for their feedback and input. Just one idea could very easily change how you work or do business.

Step 7: Find Adequate Support

The final step of this process involves finding adequate support from people who can help you get back on your feet again. You could possibly look for a debt support group in your area, or team-up with a debt elimination buddy where you both work towards the same goal.

In general, during this part of your journey, it’s important that you have the right people around you. People who splurge on their credit cards and live a luxurious lifestyle are probably not ideal company right now. However, people who consistently save their money and strive to live frugally will help you to get into those habits as well. Hang around these kinds of people and start integrating their financially savvy habits into your own life.

Seven Guidelines for Eliminating Debt

Following the seven-step process outlined above is a great way to help you get started and working your way out of debt. However, there are several more guidelines not covered within this process that you may find of value to help you get out of debt. Let’s discuss them here.

Learn to Say ‘No’

Life is full of temptations, and it’s just too easy to fall into this instant gratification trap. However, if you endeavor to get yourself out of debt, you must practice more self-discipline especially when it comes to your spending habits.

You might, for instance, be tempted to go out to dinner with your friends. However, you very well know that this dinner will set you back financially. It will be much more affordable to just stay at home a prepare a home-cooked meal. In such instances, just say NO! Don’t allow peer pressure to force you into making choices that don’t serve your best interests.

Another form of temptation comes through impulse purchases. You know what I mean, right? You go out shopping for one thing and end up bringing back a trunk load full of great bargains and items you just couldn’t pass up. 😉

Typically we get drawn into making these impulse purchases when we don’t have a budget in place. With a budget in place it’s easy to see that we can’t afford to buy these items, and therefore it just makes sense to say “no”. Getting out of debt is your number one priority. As such, anything that compromises this objective should be avoided at all costs.

Avoid Paying Recurring Fees

By “recurring fees” I mean those purchases you make that allow you to pay off an item over a period of several months or years. Often by signing up for a payment plan, you end up paying much more for the item in the long-run.

Consider that it takes you 36 months to pay off that computer you purchased. Within 24 months the processing speed of that computer will be inferior to the latest models, and yet you’re still paying off the old model.

A better approach would be to purchase the cheapest model upfront and then possibly upgrade the computer in 24 months with a better model. But the point I really want to make here is that you are playing a very dangerous game if you sign up to multiple long-term payment plans.

Budget-wise it might make sense to hold out on purchasing items upfront and instead choose to pay them off each month. However, if you do this over and over again, you will eventually get yourself into financial strife; these recurring fees will just keep piling up. And of course if you can’t pay them off, it just makes sense to dump them onto your credit card, but we all know that’s not a good idea. 🙁

Choose instead not to sign up for payment plans. Choose instead to purchase cheaper products or models that you can afford to pay upfront, or choose to purchase other people’s second-hand items. This is a far more cost-effective method and will help you to avoid getting into further debt in the months and years to come.

Take Control of Your Credit Card Spending

People typically get into financial strife because they overspend on their credit cards. However, it’s not just spending on the credit card that creates these problems. It’s sometimes the cash advances that come with a high-interest rate that really hurt us financially.

As a general rule, it’s important whenever possible to pay off the balance on your credit card each month. Paying off just the minimum amount monthly means that you will end up paying a bucketload of interest over time. And paying interest on the stuff you just bought on credit means that these items are costing you more money than you bargained for.

Yes, you saw that new suit on sale at half price and you just couldn’t resist buying it. You put it on credit because you simply didn’t have the cash on hand, however, this suit purchase has now been sitting on your credit card for six long months, and you still haven’t paid it off. So that half-price bargain you received on your initial purchase is no longer a bargain when you consider the extra interest you have paid to the bank for the luxury of using their money.

If you have multiple credit cards, it might be time to consider consolidating all this debt onto one credit card with a low-interest rate. Paying off multiple credit cards with varying interest rates will always cost you more money in the long-run than if you consolidate your debt and put everything on one card. In this way, your debt is also easier to manage.

Avoid Overpaying Your Debts

It’s important that we always take time to prioritize all the payments we make.

If for instance, you have many debts that you need to pay off, be careful not to allocate available funds haphazardly. Choose wisely to allocate funds appropriately to debts in order to eliminate unnecessary payments or interest rates.

Another thing to consider is living expenses. If you allocate too much money to paying off all your debts, then that leaves very little for the necessities. With this in mind, it’s critical to take time to think through how to best spend every dollar you earn. Yes, pay off your debts as quickly as possible, but don’t sacrifice the necessities.

Always Think Frugally About How You Spend Your Money

The best way to get out of debt is to change your spending habits. We often get into debt because we spend frivolously with no thought of the future consequences of our actions. However, with a frugal approach to spending, we take the future into consideration with every decision we make. Moreover, every dollar saved is one extra dollar that can be funneled to pay off our debts.

Living frugally requires shifting how you think about the money you spend. And the best way to start making these changes is to begin asking some pivotal questions that will help you to better manage your spending habits. For instance, asking yourself the following questions will help you to start thinking more frugally about your purchase decisions:

How can I save a little money here?

Is there a cheaper alternative to this?

How can I potentially cut out this expense?

How could I possibly reduce or eliminate these fees?

Living frugally takes time. It actually requires you make small shifts each day in how you think. In the end, it comes down to making more effective lifestyle choices that will help you to save more money and thereby pay off your debts far more quickly.

Keep Yourself Adequately Insured

When on a mission to pay off our debts, it’s easy to underestimate the importance of insurance. Insurance is something that seems like a waste of money and something that we can forgo until our debts have been paid off. However, this way of thinking can possibly lead to tremendous financial strife.

Life is unpredictable and uncertain. We simply don’t know what will happen tomorrow. Insurance covers us for these unexpected uncertainties that life throws our way from time-to-time. Yes, paying insurance monthly does hurt financially. We are effectively paying for something that we possibly might never need. But at the same time, there is a chance that it will save you from financial ruin tomorrow.

Home and contents insurance, vehicle insurance and health insurance are the three insurance policies that seem to be of most value. You can of course also throw in there life and income insurance. But for the most part, these are possibly not necessities while you are working your way out of debt.

Accidents happen, and having insurance on hand means that you won’t suddenly find yourself out of pocket and in financial strife when the roof of your house caves in, or when you’re involved in a car accident, or when you suddenly need your appendix or tonsils removed.

There is, however, another form of insurance that is not worth spending money on. That insurance comes in the form of the extra warranty you purchase for electronic items at the store. More times than not, you simply won’t need it. And if by chance your fridge breaks down, then you’ll deal with it. However, the chances are that it probably won’t happen and all the extra warranty insurance you paid for over the years could have gone a long way towards paying off your credit card debt.

Take Time to Negotiate with Your Bank

When you’re in financial strife, it’s important to gain every financial advantage you can to help you get out of debt as quickly as possible.

Consider for a moment all the fees you pay at your local bank. For instance, there are monthly account keeping fees, there are transaction fees, there are interest rate fees, to name just a few.

Banks are some of the most profitable businesses in the world. They make a living from charging you fees and interest on the money you borrow. However, they are at the same time relatively flexible and will treat each customer on a case-by-case basis. As such, it can be quite beneficial to have a chat with your local bank manager. Explain your financial situation and ask them how they can possibly help you to get back on your feet again.

Banks can, for instance, waive fees or they can potentially lower the interest rate you pay on your credit card. And if they don’t, then take your business somewhere else to another bank that is more willing and able to help you out.

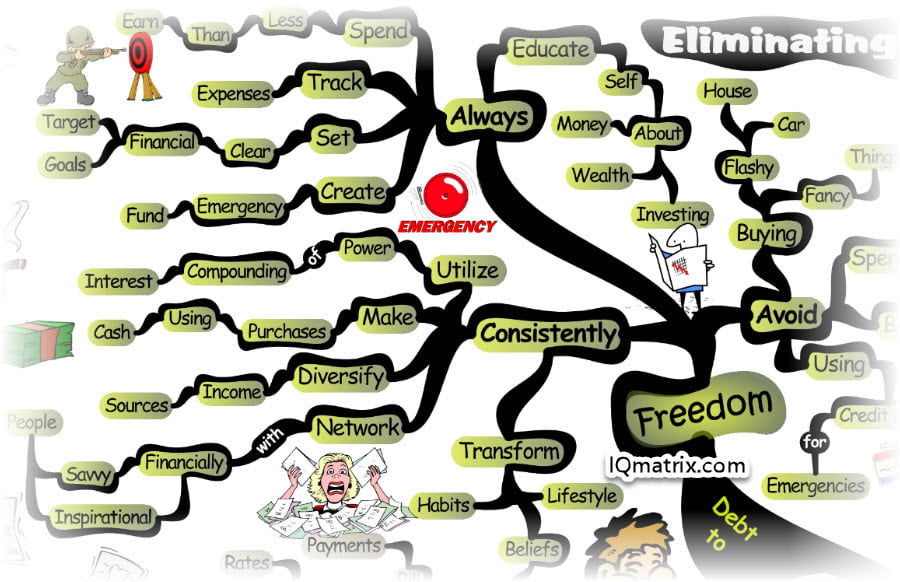

Ideas to Help You Move from Debt to Financial Freedom

Now that you’re well on your way to eliminating financial debt from your life, it’s probably a good time to talk about how to take that next step towards financial freedom.

Being debt-free is, of course, a great place to be. However, securing your financial future is essentially the ultimate goal, right? Here within this final section let’s talk about several ideas that can help you move from debt to financial freedom over the long-haul.

Continuously Upgrade Your Knowledge About Money

It is said that what we don’t quite understand we cannot effectively manage or control. This is certainly true when it comes to money. The more you know about managing money, saving money, investing money, etc, the better financial decisions you will make moving forward.

Given this, it’s important that you consistently educate yourself about money. The more you know the fewer mistakes you will make when it comes to your finances. Moreover, learning everything you can about managing money will encourage you to make lifestyle changes that will help you to create a better life for yourself and for your family.

Over time, your beliefs about money will change and subsequently, you will develop new habits that will support your financial growth and development moving into the future.

Set Very Clear Financial Targets and Goals

The road to financial freedom begins with a simple formula. That formula is of course to spend less than you earn. Once you have mastered this formula, everything else just kind of tends to fall into place. But in order to truly achieve financial freedom, you must also have a set of goals in place that helps guide your daily decisions and actions.

Set financial targets for yourself that specify for instance how much money you will save and invest in the coming weeks, months and years. Of course, make these targets realistic and achievable. Moreover, be sure to create a system that helps you track your progress, savings and spending habits over time. By knowing where your money is going helps keep you motivated and focused on achieving your financial goals.

Network with Financially Savvy People

It is said that we are the sum total of the five people we spend the most time with. Given this, if your five closest friends aren’t very financially savvy, then it’s unlikely you’re going to be very savvy yourself. As such, it’s important to start expanding your horizons and begin networking with people who understand how to manage money and build wealth.

Over time we all tend to develop the habits of those we hang around with most. Likewise, the people who are in our company feed off of our habits as well. With this in mind, it’s important to associate with people who have financial habits that you yourself would like to incorporate into your own life.

The more time you spend with financially savvy people, the more likely you are going to begin thinking like them and adopting their empowering beliefs about money into your psyche. As a result, you will begin making more effective and optimal financial decisions throughout the day.

Diversify Your Income Sources

The vast majority of people only have one reliable source of income. For many, this is normally enough to make a living but nowhere near enough to create financial freedom.

Financially savvy people always tend to have very diverse sources of income. They might, for instance, have a steady full-time job, but then on the side, they also have an online business that generates them extra income. Moreover, they have a share portfolio, a property portfolio, and possibly they even do a little coaching and consulting work on the side.

In order to begin diversifying your income consider how you could make a little extra money each week from a side business. You could, for instance, sell things online, you could become an affiliate marketer, you could launch a podcast or blog and charge for advertising, you could consult or coach, or you could produce something that solves a problem that people would be willing to pay for.

By all means, don’t sacrifice your full-time job in favor of these side income projects. Instead, choose to focus on creating other sources of income after hours one at a time. This might, of course, involve a little trial and error. Some things will work well, while others won’t. Be flexible and adapt to the opportunities that you come across, and over time you can build a nice side income business that possibly might even supplant the income from your full-time job.

Utilize the Power of Compound Interest

Compound interest is in its simplest terms the interest you earn on interest. It’s when your money grows as a result of the principal as well as the interest earned within the previous period. It could be said that it’s akin to earning money out of thin air as you grow your wealth without any additional investment or effort on your part.

To fully understand how compound interest works and how to use it to grow your wealth, it’s helpful to do a little math. That’s not a strength of mine so I will leave it up to the experts. 🙂 Please see Math Warehouse and Maths is Fun for more information.

Make Purchases Using Cash

We often get into credit card debt because making purchases on credit is just so easy. No cash on hand, no worries. Just pull out the plastic and use the bank’s money instead. 🙂

Financially savvy people do of course understand the power of credit. They will use it when needed, however, they are also wary of the dangers of spending money that they don’t have. As such, wherever possible they will tend to use cash or debit to make common weekly purchases. That way they always know how much they can spend, and as a result, tend not to overindulge on items that they simply can’t afford.

All this, of course, comes back to savvy budgeting habits. When you have a budget in place it helps you to curb your spending by effectively allocating money to very specific spending categories. A piece of software that does this very well is YNAB.

Create an Emergency Fund

An emergency fund is essentially money you put aside for emergencies such as accidents, medical fees, unexpected bills, for repairs when things break down, etc. Ideally, these funds should be placed in a separate bank account that you don’t have access to on your card.

Another important reason to have an emergency fund in place is for times when you’re suddenly out of work. Your emergency fund is designed to keep you afloat while you look for another job.

Now of course, how much money you allocate into your emergency fund depends entirely on your lifestyle and monthly expenses. Typically, we should all have at the very least 6 months of cash set aside that can help us maintain our current lifestyle without additional income coming in.

This period of 6 months allows you to regroup, to find your feet again, and to look for another source of income without worrying about how you will pay your next bill.

If however, you don’t have an emergency fund in place, then you will be tempted to make all your purchases on credit. As a result, you dig yourself deeper into financial debt by spending money that you simply don’t have. This is a vicious cycle that will keep you in debt for years to come.

Now of course, if you’re worried that you currently just don’t have the cash available for a six-month emergency fund, then that’s okay. What’s important is that you start building that emergency fund today. Allocating $25 to $100 per week is all it takes. And if you feel that you just don’t have this cash on hand, then make some sacrifices and give-up your daily coffee, or skip going to the movies and dining out with your friends. If you are willing to make these sacrifices you will find available funds to begin building your emergency fund starting today.

Avoid These Money Mistakes

We all make financial mistakes. For instance, have you ever bought big brand clothes, the newest electronics, and fancy things? Or how about spending money just to impress others? Or what about using your credit card to fund your lifestyle?

Every dollar extra you spend is one dollar less you can allocate to your emergency fund, or to pay off your debts. These financial mistakes are costly. Yes, these choices you make may not seem very significant or dire in the heat of the moment, however little choices over time accumulate and lead to some significant consequences.

In the end, the key is to think long-term. Too many of us have a short-term mentality and approach to life. We are the instant gratification generation that makes decisions based on what will make us happy today, with absolutely no consideration for the future. We should instead choose long-term happiness over short-term temporary pleasures. That is after all the only way we will get out of debt and secure our financial futures.

Time to Assimilate these Concepts

Did you gain value from this article? Is it important that you know and understand this topic? Would you like to optimize how you think about this topic? Would you like a method for applying these ideas to your life?

If you answered yes to any of these questions, then I’m confident you will gain tremendous value from using the accompanying IQ Matrix for coaching or self-coaching purposes. This mind map provides you with a quick visual overview of the article you just read. The branches, interlinking ideas, and images model how the brain thinks and processes information. It’s kind of like implanting a thought into your brain – an upgrade of sorts that optimizes how you think about these concepts and ideas. 🙂

Recommended IQ Matrix Bundles

If you’re intrigued by the idea of using mind maps for self-improvement then I would like to invite you to become an IQ Matrix Member.

If you’re new to mind mapping or just want to check things out, then register for the Free 12 Month Membership Program. There you will gain access to over 90 mind maps, visual tools, and resources valued at over $500.

If, on the other hand, you want access to an ever-growing library of 100s of visual tools and resources, then check out our Premium Membership Packages. These packages provide you with the ultimate visual reference library for all your personal development needs.

Gain More Knowledge…

Here are some additional links and resources that will help you learn more about this topic:

- 3 Simple Steps to Get Out of Debt @ Time

- 4 Tips to Help You Get Out of Debt @ ABC News

- 4 Steps to Finally Achieving Financial Freedom @ Elite Daily

- 4 Ways that Getting Out of Debt Can Go Terribly Wrong @ ABC News

- 5 Ways to Get Out of Debt While Growing Your Savings Account @ Huffington Post

- 7 Steps Anyone Can Take to Get Out of Debt @ Business Insider

- 10 Things I Gave Up to Get Out of Debt @ Huffington Post

- 14 Ways You May be Stopping Yourself from Getting Out of Debt @ Elite Daily

- A Step-by-Step Guide to Getting Out of Debt @ Lifehacker

- Study: To Get Out of Debt, Start Small @ CBS News

- Suze Orman’s Best Advice on Getting Out of Debt @ Oprah

- The Most Important Step for Getting Out of Debt @ Business Insider

- The Ultimate Guide to Getting Out of Debt @ Forbes